Markets have been volatile over the last few weeks. Global geopolitics, ongoing conflicts, interest rate uncertainty, currency movements, and mixed signals from global central banks are creating short-term noise. If you are feeling uneasy looking at your portfolio, you are not alone.

But let’s start with a simple truth.

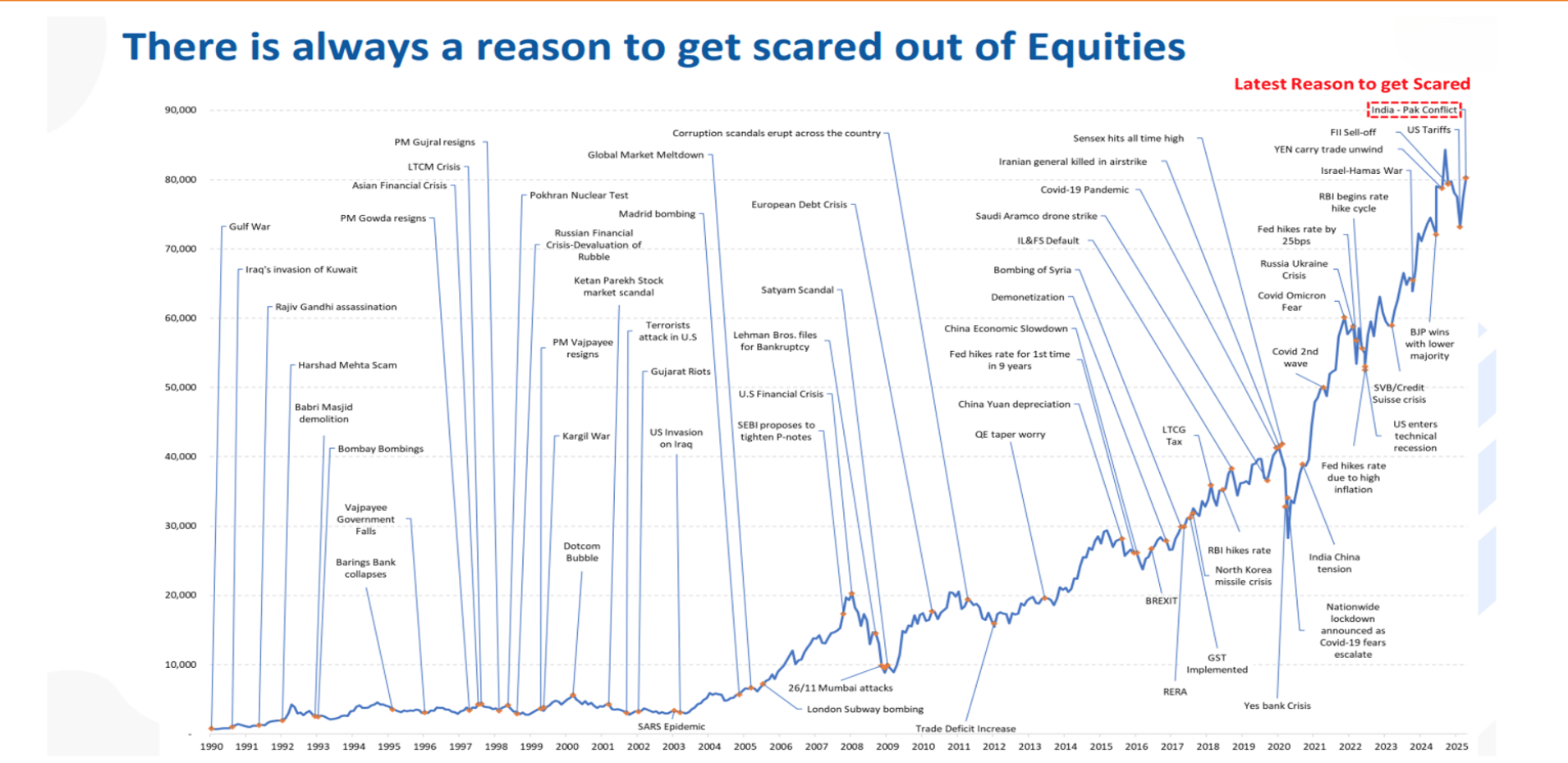

I have been tracking markets since around 1992, starting with the Harshad Mehta episode. Compared to those days, Indian markets today are far more mature, resilient, and domestically driven. Volatility feels uncomfortable, yes. But it is not unusual. In fact, volatility is the price we pay for long-term equity returns.

Indian markets are not insulated from global events. What happens in the US, Europe, China, or geopolitics closer home does impact short-term sentiment. However, India is far better placed today than it was in earlier decades.

We now have:

This domestic participation acts as a stabiliser during global uncertainty. Volatility may create noise, but structurally, India’s long-term growth story remains intact.

One of the most common mistakes investors make is reacting emotionally to market events.

Equity mutual fund investing should always be goal-based, not event-based.

We don’t invest based on today’s headlines or tomorrow’s predictions. We invest based on goals, time horizon, and asset allocation.

If you want to go deeper into this, I strongly recommend revisiting

👉 why goal-based investing matters more than short-term market movements

(this is the foundation of sensible financial planning).

Any money required in the next 2 to 3 years should not be in equity at all. That money belongs in debt or hybrid funds. Equity is meant for long-term goals, retirement, children’s education, or long-term wealth creation.

If your goal is 10 to 15 years away, market corrections are not a reason to panic. They are part of the journey.

But then, as you notice, despite all this volatility, the markets continue to rise over a longer period.

Let’s be very clear and honest.

It is unrealistic to expect that when markets fall, your portfolio will not correct. Equity portfolios will go down during market declines. That is not a flaw. It is the cost of earning higher long-term returns.

There is no such thing as “no risk but great returns.” Anyone promising that is selling fiction, not finance.

Also, portfolios should never be judged fund-by-fund in isolation. Individual funds go through cycles. What truly matters is the overall portfolio and the asset allocation designed to manage risk.Why Staying Invested During Market Corrections Matters

When markets are rising, staying invested feels easy. The real test comes when markets fall.

When we say “stay invested”, it also means:

This is where SIPs truly work in an investor’s favour. Market corrections allow you to buy more units at lower prices, improving long-term outcomes through rupee cost averaging.

If this sounds counterintuitive, it may help to read

👉 how SIPs help investors during market volatility

Those who continued investing during 2008 and 2020 understand this well today. Wealth is built through discipline during bad times, not excitement during good times.

Before worrying about returns, market levels, or portfolio performance, ensure these three basics are firmly in place. These are non-negotiable:

1️⃣ Emergency fund covering at least 6 months of expenses

2️⃣ Adequate term insurance

3️⃣ Proper health insurance

Without these, even the best investment plan can collapse due to a personal emergency, forcing you to exit long-term investments at the worst possible time.

If you haven’t revisited this recently, read

👉 why term insurance is the foundation of financial planning

These basics protect your investments so that your long-term plan can actually work.

Now let’s look at real data from our own practice, recently. This is not market theory. This is investor behaviour in action.

The message is clear:

Compounding works with time. Not with impatience.

As I keep saying, it takes 5 to 7 years for an equity portfolio to stabilise. Judging performance before that serves no purpose.

These figures reflect historical data and internal analysis at a specific point in time. Actual returns may vary based on market conditions and individual investor circumstances.

Every major correction, whether it was 1992, 2000, 2008 or 2020, felt frightening when it happened. In hindsight, each one turned out to be an opportunity for disciplined long-term investors.

Short-term volatility has never destroyed long-term wealth.

Emotional decisions have.

If you struggle with this aspect, you may find value in reading

👉 why long-term investing requires patience and discipline

Old lessons still matter. Markets reward patience far more reliably than prediction.

Instead:

There may be more short-term noise this year. Structural growth never comes in a straight line.

Stay disciplined. Stay invested. Stay focused on your goals.

That approach has worked across decades, and it still does.

Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

The information provided in this blog is for educational and informational purposes only and should not be construed as investment advice, solicitation, or a recommendation to buy or sell any financial product or mutual fund scheme.

Past performance is not indicative of future returns. Market conditions, interest rate movements, economic factors, and investor behaviour may impact returns. There is no guarantee that the strategies discussed will yield similar results in the future.

All data, illustrations, and examples are based on publicly available information and internal analysis at a specific point in time and are subject to change.

Investors are advised to consult a qualified Personal Finance Professional and evaluate their financial goals, risk appetite, and investment horizon before making investment decisions. You can know more about Financial Radiance in the “About Us” section.

You can also follow my channel www.youtube.com/c/financialradiance for more videos and shorts.