AMFI Registered Mutual Fund Distributor

A business is only as strong as its ability to withstand the unexpected.

We help you safeguard your business against risks that can’t be predicted. But can be prepared for.

Most businesses insure assets. Very few insure what truly drives value: people, partnerships, and leadership.

And when something unexpected happens, the impact is rarely theoretical.

A founder once told us, “We had profits, we had clients. But we didn’t have liquidity when we needed it the most.”

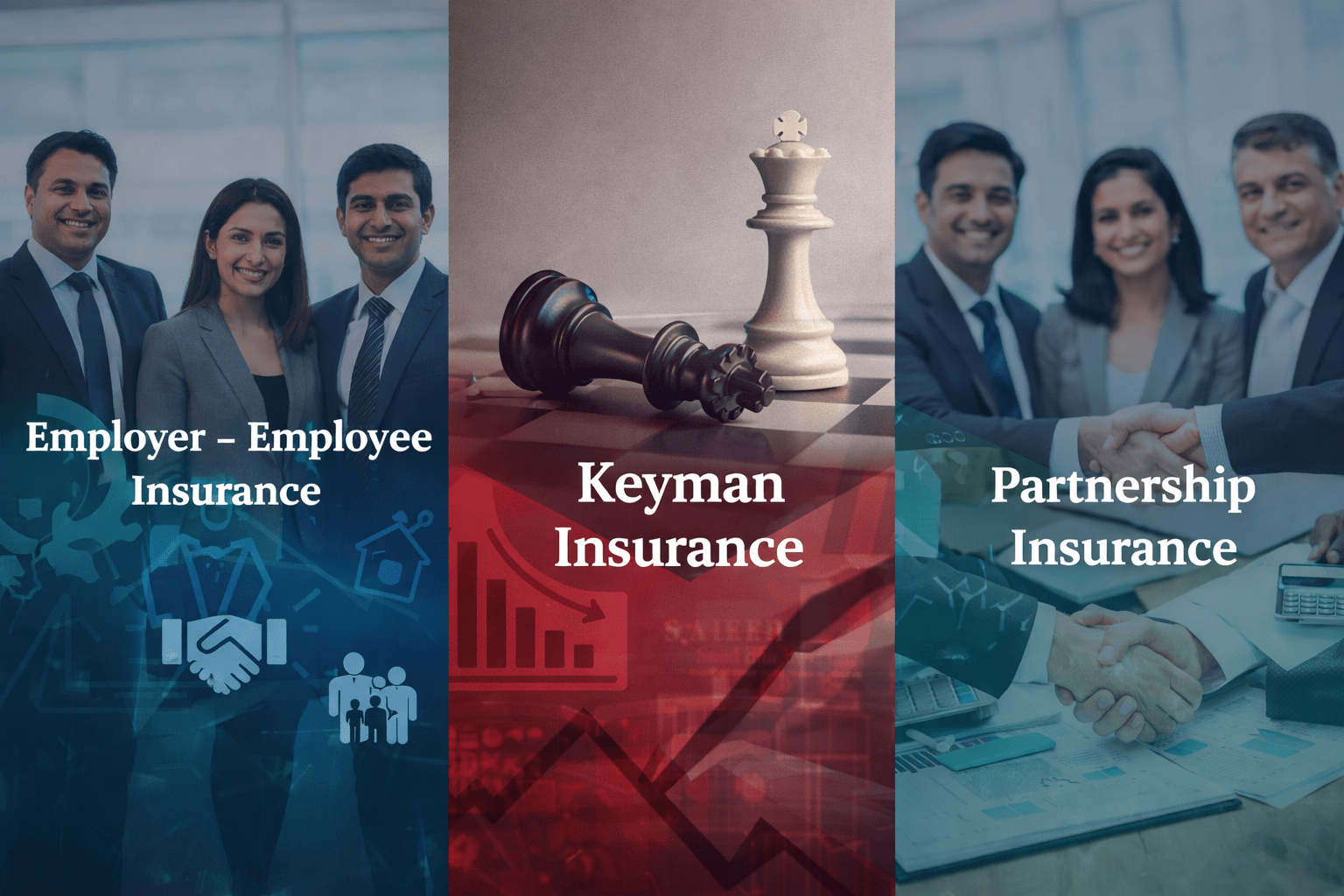

That gap is what Business Insurance is designed to address. We assist business in three types of Business Insurances.

Who is it for?

What it does

A structured solution where the business provides insurance-linked benefits to employees, aligned to tenure, milestones, or long-term value creation.

Why it matters

A growing company once struggled with senior attrition, not because of compensation, but because employees didn’t see long-term alignment.

Once structured retention benefits were introduced, the conversation shifted from “What’s my next job?” to “What’s my future here?”

• Strengthens your positioning as a serious, people-first organization

Taxation

Who is it for?

What it does

The business insures a key individual whose absence would materially impact operations or profitability.

Why it matters

In one case, a business lost a key rainmaker. Revenues didn’t collapse overnight. But pipelines dried up quietly over the next 6 to 9 months.

The real risk wasn’t the event. It was the slow financial bleed that followed.

• Buys time, something most businesses underestimate

Taxation

Who is it for?

Partnership firms and closely held businesses

What it does

Provides the financial ability to buy out a partner’s share in the event of an unforeseen loss, without disturbing the business.

Why it matters

A partnership once faced a difficult situation. The intent to continue was clear, but the funds to settle the outgoing share were not.

What followed was not a financial problem alone. It became a relationship problem.

• Brings clarity to succession when emotions are high

Taxation

Most business insurance is bought reactively.

We structure it proactively.

A business rarely fails in one moment.

It weakens when it is forced to make financial decisions under pressure.

The objective is simple:

Ensure that when something unexpected happens, money is the last thing you worry about.

If you run a business, this is foundational. Not optional.

Connect with us to structure your Business Insurance the right way.

Address

B 346, Victoria Drive, Paramount Golf Foreste,

Opp. Sector Zeta 1, Greater Noida – 201306

Uttar Pradesh

Email Address

rajeshminocha@financialradiance.com

Contact Numbers

+91 98664 61113 | +91-120-4548926